For ages I’d been playing about with

various ways to try and show the effect of bracket creep in a chart. Over the

last year or so, I’ve settled on one that illustrates the combined effect of

creep and inflation, plus whatever measures have been put place in the

tax-transfer system that add to or subtract from them. I thought the format was

reasonably self-explanatory, but when I use it for charts on Twitter I get more

than the usual number of requests to explain just what I’m trying to show.

So here goes.

First off, what kind of bracket creep am I

talking about? There’s a narrow version of the term which says bracket creep is

what happens when you have a pay increase that puts you into the next tax

bracket. Indeed, the name ‘bracket creep’ gives that impression. But bracket

creep is more than that. It also encompasses the idea that a pay increase that

doesn’t put you into the next bracket will still push you further into your

current one.

Whether your income crosses a threshold or

not, in a progressive tax system like ours a pay increase will mean

proportionally more of your pay goes in tax – your average tax rate increases. (As

an aside, ‘progressive’ in this sense means that the rate progressively rises

as income increases. It’s nothing to do with the term progressive as applied to

people open to change, new ways of doing things or reform, as in “so and so is

a very progressive thinker”.)

Here’s where we need to pause to wrestle

with a question. If a progressive tax system – and in theory, our tax system is one of those

- is designed to increase the proportion of tax one pays as income rises, why

is bracket creep an issue? It’s what’s supposed to happen, right? And if it’s

supposed to happen, if it’s doing what’s intended, then surely bracket creep is

a good thing? Alas, like nearly everything, it’s yes and no.

So, when is it a bad thing? The answer to

that rather depends on your political leanings, but I think it’s a bad thing when creep occurs even when the increase

in your income is less than or equal to the inflation rate. Such an increase is

not a real increase at all. An

increase that matches inflation means that your overall pre-tax income, in real

terms, is unchanged. However, because you’ve now crept further along the tax scale

(maybe even into a new bracket), a greater proportion of your income goes in

tax. That means your after-tax income has fallen in real terms - your standard

of living has reduced.

When I do charts that look at how things

have changed over time for a particular type of household, I almost always

compare households with the same real income. I like to see how things have

changed for identical households, separated only by time. That means adjusting

the first (earlier) household’s private income (usually earnings) to take

account of inflation, as reflected by changes in the Consumer Price Index

(CPI). For example, If I was to compare a household today, earning $50,000 a

year, with one in July 2016 (when the election for the current, 45th

Parliament was held) I would use earnings of around $48,225 for the earlier

household.

So, all this takes us to the beginnings of

my bracket creep chart. Here’s one that uses the ideas above to show how the

income tax paid by a single person household at 20 March 2018 compares to one

on 2 July 2016 (the election date for Parliament 45). All that has changed is

that the private income (eg, earnings), has increased over the period by the

CPI, or in other words, has stayed the same in real terms.

Chart 1

We can see from the chart that bracket

creep means a person earning $50,000 is worse off than their equivalent back in

July 2016 by over $300 a year. For someone earning $200,000 it’s over $1,100.

Focussing just on income tax is too narrow

though. Our hypothetical single person may also be affected by the low-income

tax offset, and where private income is low enough, or non-existent, Newstart

allowance could also be present. There’s also the medicare levy. All these

things are affected by bracket creep.

The bits of the system that are tax-like

(eg, the low-income tax offset and the medicare levy) are affected by bracket

creep in much the same way as income tax. Transfer payments (eg, Newstart

allowance) have creep effects because increases in income cause reductions in

the rate payable under the various income tests applied to transfers. They also

are affected by inflation – if the rate of, for example, Newstart allowance,

was unchanged from July 2016, not only would there be losses caused by bracket

creep, but the actual value of the payment would have fallen as well.

Given this, the obvious next step is to

modify the chart so that it’s showing the effect of creep on a wider range of

federal government tax and transfer items, adjusted for inflation. Chart 2 is

the same single person comparison, but this time taking into account the low-income

tax offset, the medicare levy, and Newstart allowance.

Chart 2

It’s still possible to see the broad

outlines of the original, income-tax-only chart, particularly at higher

incomes, but a lot of new stuff has appeared. The bigger reductions below

$30,000 are the effect of creep/inflation on Newstart allowance and to a lesser

extent the medicare levy low-income arrangements. The bulge between $37,000 and

a bit under $70,000 is the effect on the low-income tax offset. The 3 hanging

spikes are the effect of creep on the medicare levy surcharge.

As it stands, the chart now shows the

result of bracket creep on a more representative range of tax-transfer elements,

where the creep is due to private income increasing at the same rate as

inflation. It also includes the effect of inflation on the value of transfer

payments (in this case Newstart allowance). This is better, but if I was to

leave the chart in this form it would still be somewhat misleading.

Recall that the chart is based on the

effect of wage increases that match inflation, with no other changes. The ‘no other changes’ bit is a problem because

the Government may have taken steps to address creep/inflation over this

period. For example, if all the thresholds and amounts involved were indexed to

the CPI, the losses shown in the chart would be completely offset and the net

result would be that the disposable income of the household would be the same

at the beginning and end of the period, in

real terms.

Accordingly, I need to add another element to

show the effect of tax-transfer changes the Government may have made over the

period. And so to Chart 3

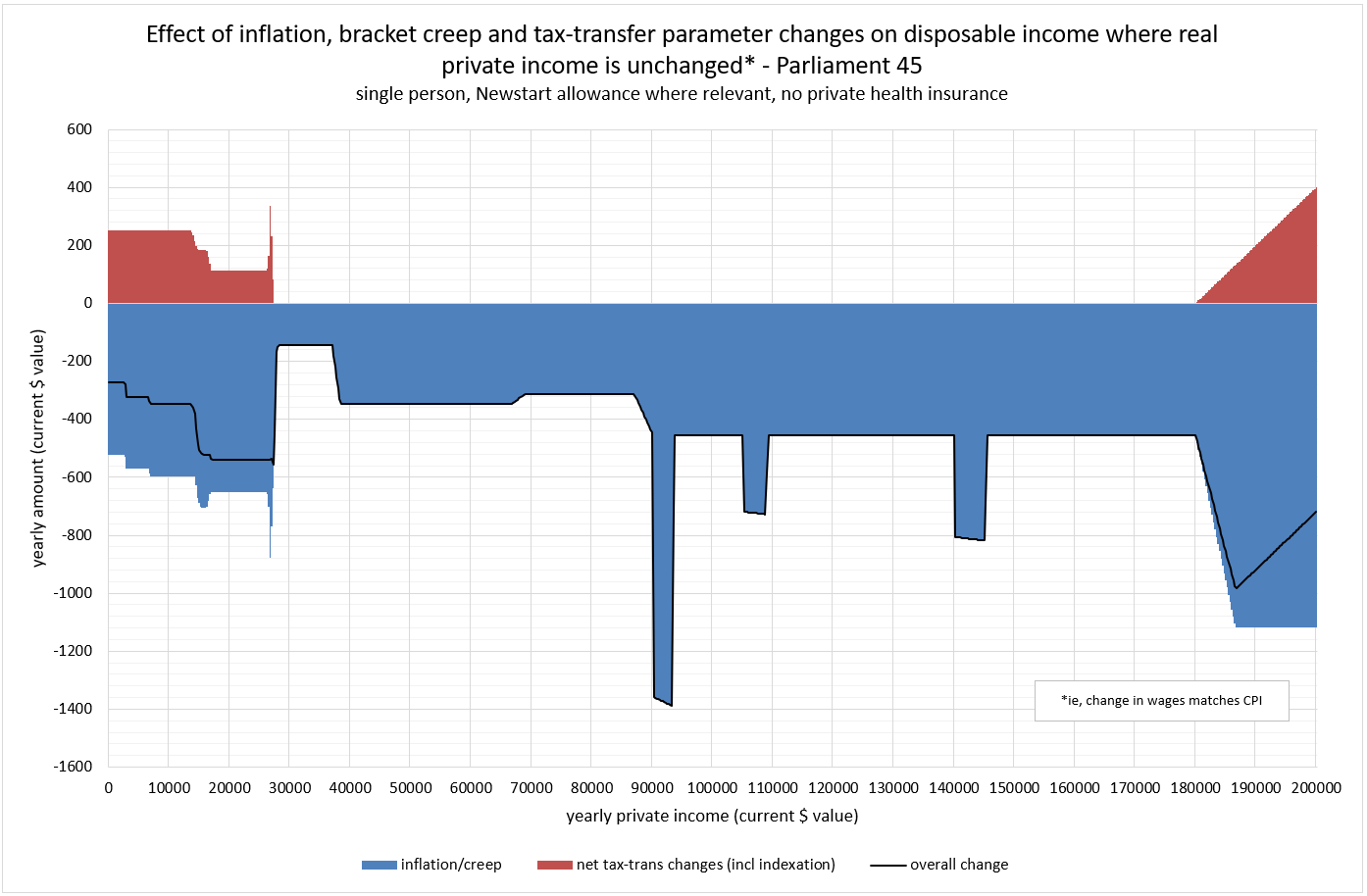

Chart 3

The red areas on the chart show the effect

of the Government’s changes to the tax-transfer system over the period – in this

case since the election of the current Parliament (Parliament 45). Between

approximately $30,000 and $180,000 there have not been any, so the reduction in

disposable income from bracket creep remains as it was in Chart 2.

Above $180,000 there has been some offset to

the creep effect. This is a result of the ending of the budget repair levy, originally

imposed during Parliament 44 and which applied only to those with incomes above

$180,000. Below $30,000 we can see that something happened to offset creep and

inflation, but, as the black ‘overall change’ line shows, only partially. That ‘something’

was the regular inflation adjustments to Newstart allowance. It didn’t

completely offset creep and inflation because these adjustments are not being

applied to the entire Newstart allowance and, more substantially, the

Government also abolished the income support bonus.

These finer details – which bits of the tax

transfer system are affected and by how much – are not discernible from this

type of chart and I didn’t intend that they would be. My intention was for the chart

to show the change in disposable income due to inflation/creep for households whose gross private income

has remained the same in real terms; what further effect (additive or

subtractive) Government changes have made; and the net result.

If you are keen to see charts that have

more detail about what parts of the system changed and by how much, I do have

something along those lines. Chart 4 is an example, which also uses the same single

person household we’ve been looking at.

Chart 4

This gives the same overall result as shown

by the black line in chart 3, broken down by component. There are more of these,

and other charts, on my ‘collection’ post here.

RAVE BY DAVE THE RAVE NO1RAVER NORTHEAST LEGEBND ALL ABOUT RAVE

ReplyDeleteyes alll about rave by dave the rave no1raver northeast legend keeping the rave alive rave heaven

ReplyDelete