I also thought I'd retain the comparison with earlier governments, and add in an extra one for good measure. So, in this post I'll include the results for the last 4 governments - Parliaments 40 to 43 inclusive - being the last 2 Howard governments, the Rudd-Gillard goverment, and the still-in-train Gillard government.

As before, this is for a single person who has not taken out private health cover (I want to be able to show the effect of the medicare levy surcharge).

The first chart is a spaghetti effort. It shows all 4 governments and the percentage change in disposable income over the term of each. This is measured in current dollar terms (ie, it's CPI adjusted).

(click to enlarge)

It's a bit hard to make out really, but the last Howard government really stands out at both ends of the income range I've covered here. In contrast his preceding period was quite lackluster. Let's have a closer look at that one (Parliament 40).

(click to enlarge)

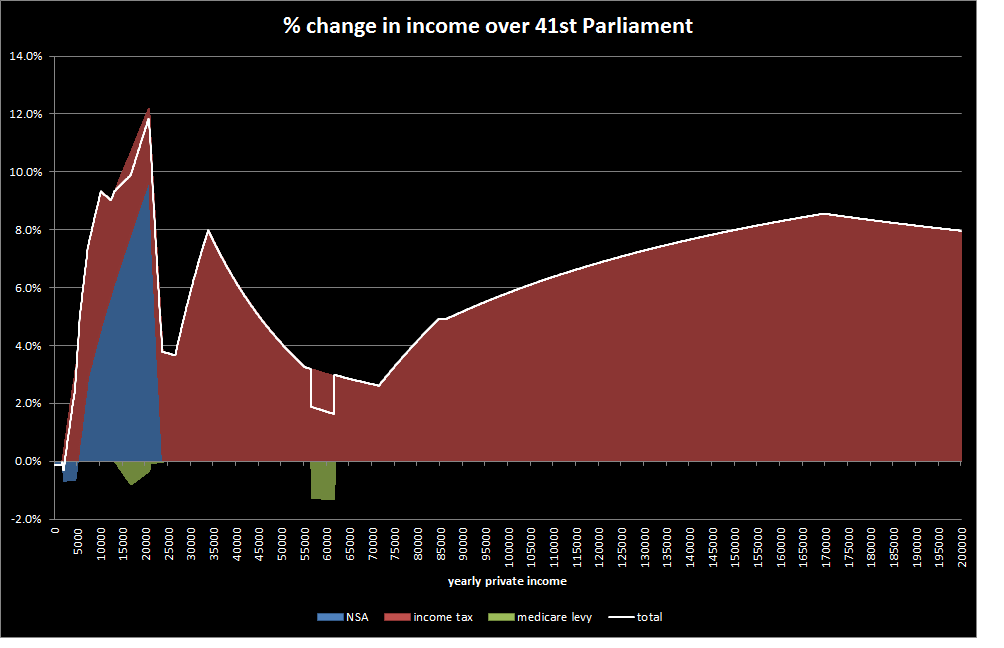

This chart shows the contribution of the individual tax-transfer elements that go to make up the total change - tax, medicare and (at low incomes) Newstart allowance (NSA). At the low income end we can see that NSA declined in value where it was combined with some level of private income. This reflects that fact that the NSA income test parameters were not changed during this government and so declined in value in real terms. There are some tax changes and a bit of medicare movement (the dip at around $60,000 is, like the NSA decline, due to a lack of indexation of the surcharge threshold). Overall though, the whole thing is easily contained within a 2% up or down band.

In the following term, the brakes seem to have come off...

(click to enlarge)

In this period there were a succession of tax cuts (those on 1 July 2006 were particularly large). These favoured the higher income end, but there were equally generous (in proportional terms) cuts at around the $35,000 mark. Interestingly, NSA recipients who had some private income had a significant boost to their incomes as a result of a relaxation of the NSA income test tapers.

The election campaign at the end of this Parliament had the intriguing spectacle of both Labor and the LNP coalition offering very similar tax cuts if elected (Labor's were quite explicitly designed to almost exactly match the LNP proposal). In the event, Labor was elected and the promised tax cuts were duly delivered.

(click to enlarge)

A couple of things to note here. The decline in the NSA rate even at zero income is actually a product of the timing of CPI increases to the NSA rate relative to the election dates. NSA is CPI indexed and so in theory it's maximum value (at zero private income) shouldn't change in this type of chart. However, the actual date of the increases in rates lags a little and so the rate wobbles around the no-change position rather than nailing it every time. This is only true of the maximum rates though - the declines where there is also some low private income reflects the lack of any indexation or other changes to the NSA income test. The other item is the medicare levy surcharge - in this period there was a significant increase in the threshold at which the surcharge applied, with the resultant (green) boost to incomes in the affected income range.

So now to the current government. After 8 years of quite noticeable increases in incomes in real terms just from the tax-transfer system (ie, ignoring any wages growth or other factors that contribute to household prosperity) we have this:

(click to enlarge)

It's a bit like Howard in Parliament 40, except that it's the higher incomes that have gone backwards rather than the low income end. There has been a noticeable increase for low income singles due to the combination of clean energy payments and tax cuts, but this has disappeared by $40,000 - the cuts don't make up for the effect of inflation.

On the subject of inflation, it's worth noting that the effects of carbon pricing have yet to appear. Without other changes to the tax-transfer system, when they do flow through the results above will be pulled down even further.

To me the results to date for Parliament 43 (remembering there's still over a year to go) go some way to explaining the perceptions of a decline in incomes that keeps bubbling away in the media. Sure, wages growth will override this, and declining interest rates will too. But not for everyone - those on fixed incomes, and those relying on interest income are not helped. And even for those who do benefit, they are having to come off a lower - and negative - base compared to the two preceding Parliamentary terms.

I like these forays into comparative Parliaments, so I may do some more down the track with other household types. If there's one that interests you let me know in the comments.

Cheers!